By George R. Pilcher, The ChemQuest Group, Inc.

Raw materials, in the form of individual chemical constituents that are incorporated into paints and coatings, represent an exceptionally diverse and vitally important sub-set of the overall specialty chemicals industry. They may either be added to a paint or coatings formulation during the product manufacturing process—or, in the case of multiple-component coatings systems (2K, 3K, etc.)—may be used to make coating components intended to be combined in the field to produce reactive, limited potlife products.

Coatings raw materials can be grouped into four broad categories of chemical constituents:

Resins: Polymers either dissolved—or carried—in water or organic solvents

Pigments: Both chromatic (“primary pigments”) and extender, filler, flattening, etc. (“secondary pigments”)

Solvents: Organic—water is not discussed in this article

Additives: Rheology modifiers; surfactants; dispersants; biocides; coalescents; catalysts; defoamers; adhesion promoters; and a host of other specialized chemical constituents typically used at very low levels, as a percentage of the formula weight

The global coatings raw material market is estimated to be valued at approximately $63.5 billion on 34.3 million metric tons of materials.

Raw Materials Market Analysis

Raw materials used in the manufacturing of paints and coatings represent a relatively small (~5%) but extremely important component of the $4.5 trillion global chemicals industry. All of the world’s leading chemical producers are active in the coatings market, and many coatings raw materials are used in other industries as well, including plastics; synthetic lubricants; adhesives; sealants; household, industrial and institutional cleaners (HI&I); personal care products; paper; plastics; water treatment and many others. The basic chemical components that are used to produce coatings chemical constituents can also be used to produce a wide array of other chemical compounds. This can be a problem at times, since this diversity of uses can create competitive situations for raw materials and their pre-cursors that are typically used in coatings, particularly during periods of tight supply.

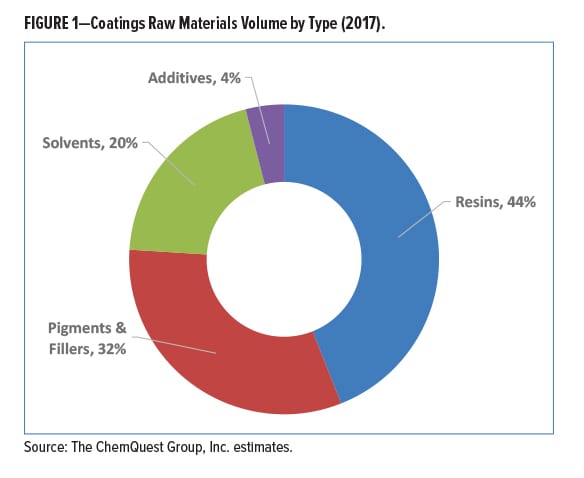

Resins (“binders”), pigments, and fillers represent over 75% of the global coatings raw materials market. Figure 1 shows the estimated distribution of coatings raw materials volume by type.

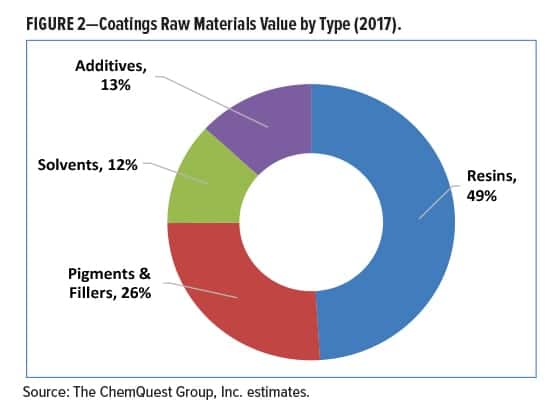

As might be readily anticipated, the distribution of the types of raw materials, based upon value, is somewhat different than distribution based on volume. Figure 2 shows the estimated distribution of coatings’ raw materials value by type.

Resins

Total global sales of resins for use in coatings systems are estimated to be $31 billion on roughly 15.2 million metric tons.

Globally, acrylic resins are the most commonly used binder in paint and coatings systems. This is particularly true for decorative paints, and includes all acrylics, both pure and modified, such as styrene-acrylics and vinyl-acrylics. It is estimated that acrylic systems, both solventborne and waterborne, comprise approximately 27% of total coatings binder demand. It should be no surprise then, that acrylic resins tend to be the most susceptible to periodic disruptions in supply, accompanied by price fluctuations. In 2017, for example, shortages of methyl methacrylate (MMA), due to a variety of causes, including a shortage of acetone and two major U.S. suppliers of MMA being down (for different reasons) at the same time, led to nearly monthly increases, with MMA climbing roughly $0.50/lb, from “mid-$0.80s/lb” in February 2017 to “mid-$1.30s”/lb in January 2018. Prices on both the spot market and the black market during 2017 were reported to be “sky high.” While supplies are somewhat more stable going into 2018, price increases were announced for both January and February, and there are still likely to be additional increases.

On a global basis, alkyds are used to some degree in virtually every end-use coatings segment, and represent the second most common type of resin system used in coatings formulations. Alkyds comprise roughly 20% of resin demand in the global coatings market (≤10% in the United States). Although alkyd resins have been steadily declining in use, particularly in North America and EU, as VOC limits continue to drop, and the market has been moving to other resin types for water-based and higher-solids formulations, newer water-based alkyd systems are being introduced into the market, at least in part due to the increasing interest in resins made with higher renewable resource content.

Polyurethane coatings, either 1K, 2K (or occasionally 3K) are widely used in the automotive OEM, other transportation, automotive refinish, wood, industrial finishes, decorative coatings and even severe-service marine and high-performance industrial segments. Urethane resins currently comprise roughly 21% of the global demand for resins in coatings. Usage of polyurethane resins has been growing over the past several years due to their performance properties and their ability to be used in lower VOC formulations. An important, and growing, sub-segment of polyurethanes in the United States is 2K polyureas. To comply with increasingly stringent VOC requirements, polyurethane waterborne dispersions (PUDs) have been developed and used to formulate single-component coatings with improved abrasion resistance compared to waterborne acrylics. They can also be combined with other waterborne resins to meet cost targets and performance needs.

Approximately 16% of total demand for binders used in coatings is supplied by epoxy resins. Various resins in the epoxy family are widely used in electrodeposition (ED) coatings and in industrial coatings, particularly in the transportation, industrial maintenance and marine markets. Epoxy resins are also widely used in powder coatings. In recent years, high solids and ultra-high solids formulas using liquid epoxy resin dominate and continue to grow. Liquid epoxy resin is also used for 100% solids epoxy formulas applied as concrete surfacers, tank linings, and for other select applications, often augmented with phenoxy and novolac resins to enhance certain performance features. While the performance of waterborne epoxy resin technology has improved, even accounting for higher consumption due to its improved performance, it has only attained a small technology share, albeit with major usage in metal can coatings. These are, however, coming under increasingly close scrutiny in the United States, where BPA toxicity concerns continue.

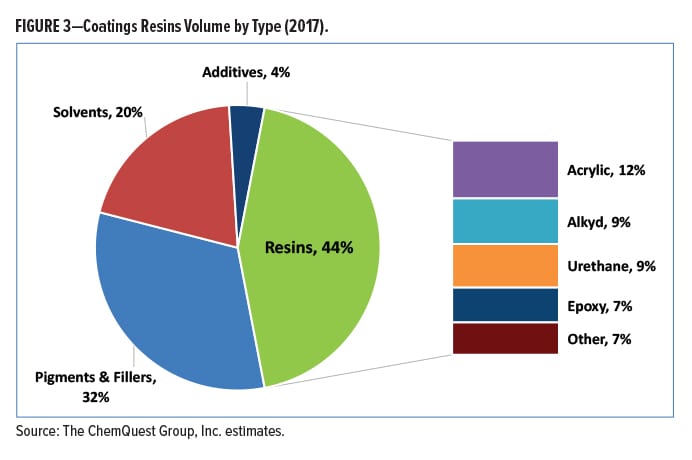

Additional binders that are used as coatings raw materials include amino, polyester (with low-bake versions as the growth area), cellulosic, silicone/polysiloxane, silicate and vinyl resins. Fluoropolymers are another interesting type, with waterborne versions now being offered for high-end architectural exteriors and other applications. Also included in this sub-segment are hydrocarbon resins and natural resins such as rosins and shellacs. While technically not resins, linseed oil, tung oil and similar products are also included since they act as film formers. This sub-segment comprises approximately 16% of total resin demand in the global coatings markets. Another small but growing resin chemistry is that of radiation cure, with the current greatest volume used in wood and plastic coatings—where sometimes even dual WB/UV cure technology is used. See Figure 3 for a breakdown of the major resin types.

Pigments

The value and volume of pigments, both primary and secondary, for use in coatings formulations were estimated to be $16.5 billion on 11.0 million metric tons of product. On a volume basis, fillers and extenders are the largest sub-set of the pigments category and represent roughly 56% of all demand for pigments in the coatings market. Compounds that comprise this sub-segment include clay, calcium carbonate, talc, silica and other inorganic materials.

The second largest sub-set of the pigments category is titanium dioxide (TiO2), which is the single highest-volume pigment used in coatings. Its largest use is in decorative coatings, but it is widely used in a variety of industrial OEM coatings and industrial maintenance/protective coatings, as well. Titanium dioxide represents approximately 31% of all pigments used as coatings raw materials, and this is likely to be somewhat problematic in 2018, with Q1 lead-times of 60–90 days, and scattered instances of allocation as well. The global economic climate currently favors all market segments that use TiO2, most notably the building and construction segment. This will, therefore, be a year of continued price increases, which could easily take TiO2 as high as $3100/mt, albeit still significantly short of its 2011–2012 historic high price of ~$4500/mt. Increases in Chinese chloride-process TiO2 production are essentially being offset by continued closure of sulfate-process plants, and Huntsman’s plant in Finland is not scheduled to be back to full production until the end of 2018. If the acquisition of Cristal by Tronox is finalized (the U.S. Government filed a complaint aimed at stopping the deal on December 5, 2017), it is unlikely to unleash any additional pigment into the market during 2018, although might be reasonably be expected to add an additional 100Kmt to global output in subsequent years.

For certain end-use applications such as decorative, automotive OEM and automotive refinish, color is a primary driver of product selection. Hence, color pigments play a vitally important role in the coatings industry. Despite the importance of these materials, color pigments represent only a small component of pigment demand. Included in this segment are both inorganic and organic pigments. Inorganic color pigments such as iron oxide are the most frequently used and represent over 80% of the volume of color pigments. Organic color pigments are among the highest-priced raw materials and, thus, despite their relatively low volume, represent a significant portion of the market value. Organic color pigments are likely to increase 3–4% in 2018, as a result of competition for the basic chemicals from which they are built, and that largely come out of the AP region—production of which can be affected at almost any time as the Chinese government becomes increasingly proactive about shutting down chemical processes in an effort to improve air quality. Complex inorganic color pigments (often referred to as CICPs or ceramic pigments) are growing in importance because they meet the higher performance demands of chemical inertness and heat stability, along with lightfastness and excellent weathering properties. Moreover, with only a few exceptions (such as perylene black), CICPs comprise the majority of IR-reflective pigments that now enable formulation of various colors with energy efficiency properties. Color pigments represent >6% of the volume of all pigments used in coatings.

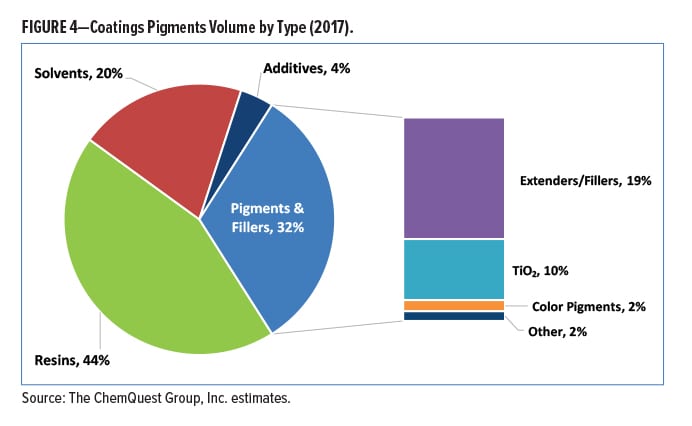

In addition to the pigments listed above, there is a wide array of other specialty pigments, such as anticorrosive pigments, metallic pigments, pearlescent pigments, carbon black and zinc oxide. While some of these pigments play an important role in coatings volume, none individually represents a significant volume. These other pigments represent roughly >6% of the total pigment demand. See Figure 4 for a breakdown of the major pigment groups.

Solvents

Solvents are the key contributors to the volatile organic content of paints and coatings emitted into the atmosphere and, as a result, are regulated by various local, regional, state and country regulatory agencies around the world.

Global revenues for solvents used in coatings formulations in 2017 were approximately $8 billion on 6.5 million metric tons.

Oxygenated solvents comprise over 60% of demand within coatings formulations, and include chemical components such as alcohols, ketones, esters, glycols and glycol ethers. Hydrocarbon solvents are either aliphatic or aromatic and comprise less than 40% of total usage within coatings formulations. As a result of the continuing shift in paint and coating formulations from solvent-based to water-based technologies, ultra-high solids and 100% solids, overall usage of solvents is declining as a percentage of the total coatings raw materials usage. While solvent usage as a percentage of total raw materials continues to decline, however, many end-use segments that use solvent-based coatings continue to grow. As a result, total solvent usage has been relatively flat over the past decade or so, and this trend is expected to extend into the foreseeable future. Similarly, within the solvents family, shifts are ongoing as formulators seek to find less toxic and more compliant, environmentally friendly solvents. Unfortunately, VOC regulations—and the concept of “what is exempt and what is not”—differ around the globe. For example, 2,2,4-trimethyl-1,3-pentanediol monoisobutyrate (“Texanol™”), historically the most effective coalescing agent for latex paints, is listed as non-exempt by the U.S. Environmental Protection Agency, but in the EU it is listed as exempt. This can make formulating “global coatings formulations” anywhere from tricky to impossible, depending upon the coating, application, and performance requirements.

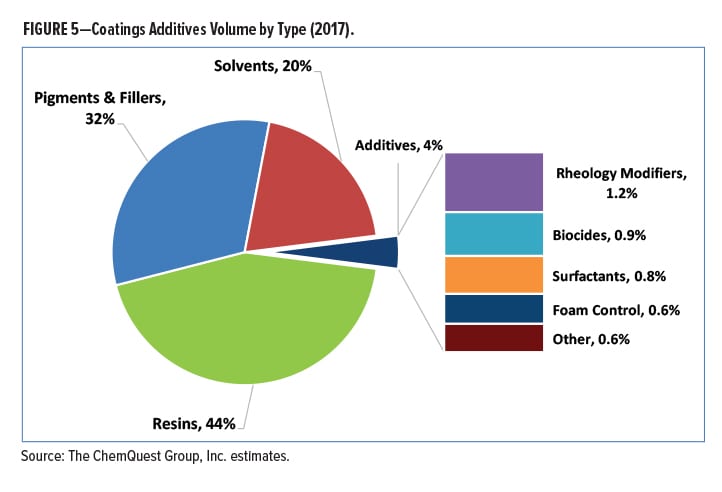

Additives

Additives comprise a broad category that covers a wide array of chemicals used as raw materials for coatings. Recent innovations include multi-functional additives to simplify the number of formula ingredients and also include those that help to achieve low- to zero-VOC formulations. Total revenue for additives used in coatings is estimated to be $8.4 billion on approximately 1.25 million metric tons.

Rheology modifiers are the largest sub-segment, representing over 30% of demand, and are used to control viscosity and to affect flow and leveling. Plasticizers are incorporated into formulations to improve the flexibility of the film, and may also be used at times for their coalescent properties. Biocides are added to formulations to prevent the growth of bacteria and other microorganisms while the coating is being stored, and also as a dry film preservative. Biocides, including special chemical components that are used to minimize marine fouling, comprise approximately 22% of total additives used in coatings. Surfactants represent approximately 19% of additive demand on a volume basis, with foam control additives at 15%.

The list of other additives is quite long. While none represents a significant component of coatings raw materials individually, “Other Additives” collectively comprise a significant portion of all additives and include adhesion promoters, antifoaming agents, anti-skinning agents, corrosion inhibitors, driers, flatting aids, flood control agents, sag control agents, slip aids and UV absorbers, to name a few. See Figure 5 for a breakdown of the major functional classes of additives.

Regional Distribution

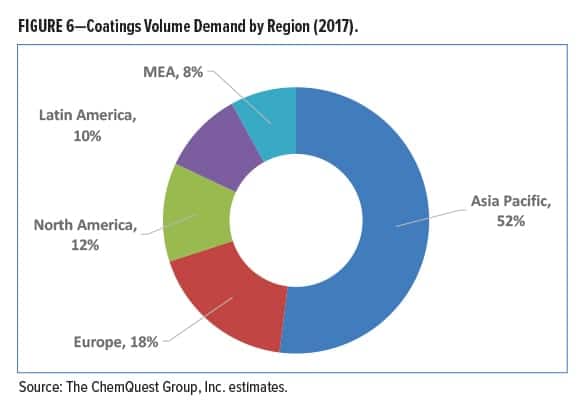

Globally, regional distribution of coatings raw materials generally follows overall production of coatings. Figure 6 depicts total global demand for coatings by region.

Competitive Landscape

The competitive landscape is quite complicated. In general, there are three types of competitors that operate in this market:

The first type of competitor is large, multinational chemical companies serving many industries that compete across coatings raw material categories. Examples include:

- BASF

- Celanese

- Allnex

- DowDuPont

- Eastman Chemical

- Evonik

- Huntsman

- Lanxess

- Momentive

- W.R. Grace, et al.

Large, multinational chemical companies play a significant role in the coatings raw material market and command a considerable share of the raw material demand. The scale, degree of integration and broad product portfolios of these competitors are perceived as key advantages. Merger and acquisition activity among the large, multinational chemical companies has had a significant impact on the coatings raw materials market, and acquisitions are forecast to continue. Private equity firms continue to show an interest in acquiring raw materials suppliers.

The second type consists of multinational product specialists that focus on a limited product offering. These companies tend to specialize in a specific product or chemistry niche(s), and are frequently innovation drivers in the market. Competitors of this type vary widely in size, based upon geographic scope, product breadth and market focus. Examples include:

- Cathay (pigments)

- Heubach (pigments)

- Nubiola (pigments)

- Alberdingk Boley (W/B resins)

- Reichhold (resins)

- Worlee-Chemie (resins)

- ALTANA (BYK—additives)

- Troy Corporation (additives)

- Michelman (additives)

As is the case with multinational chemical companies, mergers and acquisitions are anticipated to continue, impacting the specialist competitors as they are acquired by either larger chemical companies to complement their portfolio, or by other specialists to gain scope and share.

The final type of competitor is the local/regional suppliers. These generally focus on a limited product offering. Examples among the numerous local/regional suppliers:

- Optimal Chemicals

- Organik Kimya

- Silberline Synthopol

- Specialty Resins

- OPC Polymers

- Orion Engineered Carbons

- Many, many others

While none of the local and regional suppliers have significant share on their own, collectively they are an important source of coatings raw materials. Competitors in this group offer an assortment of value propositions tailored to their customer mix. In some cases, due to lower overheads, local/regional suppliers are able to provide lower cost alternatives to the major suppliers. In other cases, they are able to provide unique products or services that allow them to effectively compete. Significant consolidation is anticipated among this group.

Market Trends and Drivers

End-Use Markets

Demand for coatings raw materials is directly linked to coatings demand. Over the coming five years, demand for coatings is anticipated to grow at a rate of 4–5% annually. This would result in a 2022 demand for raw materials of approximately 42 million metric tons. Asia Pacific is forecast to experience the greatest volume growth (5–6%) to 2022. Europe is likewise forecast to experience moderate growth of perhaps 3–4%. North America is forecast to post somewhat more robust growth of 4–5%, but the exact mix of raw materials consumed within each region will depend on specific end-use market growth.

Economic Influences

Significant numbers of raw materials used in coatings formulations are either derived directly from oil for their chemical composition, or indirectly as a result of energy derived from oil for their mining and/or processing. The price of oil can be highly volatile and many factors can impact this forecast, driving the price/barrel either up or down. As a result, oil prices have a significant impact on the price of coatings raw materials. ChemQuest estimates that there is a “pass-through factor” of roughly 50%—i.e., if the price of oil doubles, raw material prices will increase by 50%. A realistic worst-case scenario might see prices of crude oil 50% higher than the forecast, which would increase raw materials for paints and coatings roughly 25%. Over the coming five years, the price of oil is forecast to remain relatively stable, within the range of $60–$70/barrel according to the U.S. Energy Information Administration (EIA). The implication for raw material suppliers and coatings formulators is that the price of the base materials that comprise coatings will likely rise at a rate similar to the rate of inflation to 2022.

This article was published in the May issue of European Coatings Journal and was reprinted with permission of the publisher.

CoatingsTech | Vol. 14, No. 5 | May 2018